Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

May 1, 2018

The stock market’s response to the reporting on first quarter earnings over the past few weeks shows that January was likely the moment of peak happiness for investors in this cycle. The earnings results so far have been exceptional, and Wall Street is running out of superlatives to describe them. Roughly 80% of S&P500 companies have beaten consensus earnings forecast, versus the historical average of 64%. These beats are driving first-quarter profit estimates higher. At the start of the year, analysts expected a 12% growth rate and this steadily increased to 18%, including the impact of the U.S. tax cuts announced in December. That number now looks like it will com in around a 22% growth rate, with more to come over the rest of 2018 as the tax cuts work their way through. Yet investors have been unimpressed. Since earnings began with the big bank reports on April 13, the S&P 500 is up just 0.2%. The earnings season started off quietly with the big banks beating expectations on surprisingly strong trading revenues from the likes of Goldman Sachs and Morgan Stanley. But investors were less impressed with slower loan growth at Citi, JP Morgan, Wells Fargo and Bank of America, and so the stocks drifted lower.

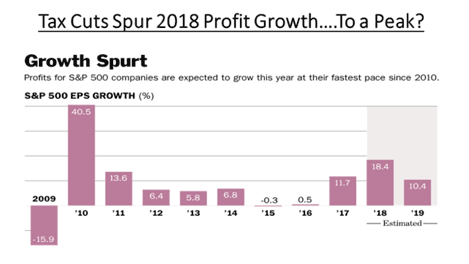

While good numbers continued to roll in across most industries, stock investors have been extraordinarily critical of what they’re being served. Take Caterpillar, which initially rallied after reporting better-than-expected results. But, on the post-earnings conference call, its chief financial officer suggested that the first quarter could be the “high-water mark for the year,” as margin improvements would be tougher to achieve. That comment immediately set off alarm bells with investors. If it doesn’t get any better than that, the stock market’s response isn’t to savor the moment, but to sell it. CAT ended up losing 6.2% in reaction to that comment, leading a massive retreat in industrial and material names that helped the Dow industrials reverse from a gain of over 200 points to a loss of over 400 points in that trading session. Stocks finally got a reprieve with another blow-out quarter from Boeing and surprisingly strong numbers from tech giants Intel, Texas Instruments, Microsoft, Facebook and, of course, Amazon, which have all benefitted greatly from their migration to cloud-based businesses. All those companies handily beat expectations on both the top and bottom lines and also raised guidance for the balance of 2018. Stocks then rallied and recovered most of the early ‘reporting season’ losses to finish mostly unchanged. But the Caterpillar comment has clearly made investors wary as they look at the entire market and think ‘was the first quarter the high water mark’ after all? We know that the tax cuts are adding about 8% to the quarterly growth rate of earnings for each of the next four quarters, but then those gains will fade away. Where then will earnings growth come from if profit margins have peaked, input costs are rising, economic growth slowing down and the impact of the tax reductions falling away? The chart below shows the annual earnings growth since the Financial Crisis. If this is indeed the peak year for earnings growth then recent stock price action may just be a reflection of the worries about what comes next!

Peaks in earnings growth are usually accompanied by stock market turbulence. The current ‘bottom up’ sell-side consensus implies a peak in earnings growth in the third quarter of this year, followed by more moderate, but still positive, growth in 2019. History suggests this would be a problem for stocks. When growth rates for S&P500 earnings peaked in 1993, 2004, and 2009, the index was lower six months later. Investors have been facing this conundrum lately as they now have some trade-offs they have to deal with. A good economy and fiscal stimulus means stronger economic growth and rising earnings, boosted further this year by the tax cuts. But it also means a determined U.S. Federal Reserve which will continue raising interest rates and growing fiscal deficits mean a very heavy supply of Treasury paper to fund them, thus adding to an already suffocating debt. Full employment and rising commodity prices are also leading to cost pressures on companies, which are starting to show up in reduced profit margins. Meanwhile, stocks are at a point where their valuation cushion against corporate bonds is as thin as it’s been this bull market.

This doesn’t necessarily mean the bull market is over, but the upside to the old highs and beyond would need something stronger than current projections. Rebounds in recent months have been unimpressive with volumes on ‘down days’ exceeding those on ‘up days’, declining market breadth and a growing list of new 52-week lows. The “sell-the-news” response so far to good earnings will continue to keep investors off balance. That isn’t an entirely irrational response, given data that show growth is slowing, while inflation is picking up. Add rising rates to the mix and we can see why stock market volatility has picked up since the February sell-off. This bull market in stocks is in its late stages and we may have already put in the highs for this cycle. But there will probably be enough earnings gains this year to bring buyers back in at some point. The flood of new money has continued due to low global interest rates and an improving economic backdrop. But the stock market is a ‘forward looking’ entity and its next moves will be determined by economic and earnings growth later this year and into the next two. The strong stock market gains of 2017 were in anticipation of the good earnings growth we are seeing now. There are more headwinds building up against a continuation of that trend and that is what stock investors are struggling with.

In terms of the early impact of tax cuts on economic growth, they don’t appear to be headed into the right ‘pockets’. Companies were intended to use the windfalls of money to stimulate growth and employment by increasing capital spending and employment. Instead, they are using proceeds from corporate tax cuts to continue the practice of rewarding shareholders and executives over workers. In the first quarter of 2018, corporate America dedicated $305 billion to stock buybacks and cash takeovers compared with $131 billion in pre-tax wage growth, according to TrimTabs. Before the tax cut, U.S. companies were spending far more money on cash mergers and stock buybacks — actions that tend to boost disproportionately the compensation of top management — than on hiring new workers and paying more to existing workers. Companies committed $4.9 trillion over the past five years to buybacks and deals, pessimistically defined as “financial engineering,” while they spent $2.3 trillion to wage increases! Corporate executives are clearly putting their company’s stock market performance ahead of larger economic growth initiatives. Supporting stock prices at the expense of improved economic growth is not a winning formula for the long term, although it can reward investors in the short term and keep existing management comfortable in their positions.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.